It’s all my fault. Stats are late and I apologize, but I had the most amazing vacation…a week on a raft on the Colorado River IN the Grand Canyon. Epic. Go do it.

In reviewing the news and the reports I receive regularly, the data in this report doesn’t exactly match up to the doom and gloom that they are selling out there. I even emailed constructive criticism to the writer of a piece I read. Turns out he was the owner of the publication and he admitted to me that clickbait and overly sensationalized article titles are what keeps him in business. We will try to avoid those things in this modest publication.

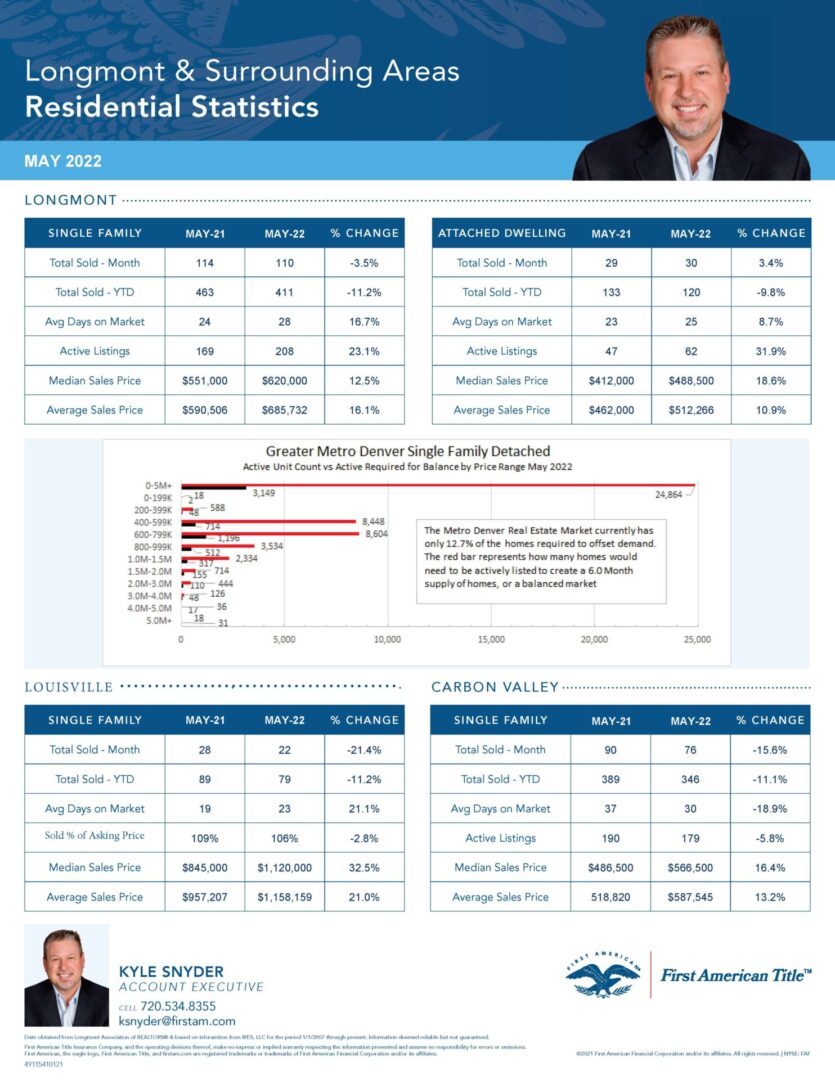

First, please look at the graph with the red and black bars. I stole this fair and square from First American’s stats guru down in Denver. Her name is Megan Aller, and she is much smarter than me. I know this graph shows Metro Denver stuff and that isn’t quite us up here in the Longmont area, but the data is representative of the whole state if not the whole country. Inventory is an issue, and we all know it, but this shows the enormity of the problem. Bottom line: it says that if Metro Denver added 24,864 listings today, we’d have a balanced market (6 Months of inventory). If you think things are bad now, try seeing it for what it is – less awesome than it was a few months ago. As inventories start to grow, the market will actually look more normal. It’s a long, long, long way from bad.

We sales reps are getting a lot of requests for agents to receive our foreclosure list every week because they still believe the foreclosure tsunami is coming. It’s not coming but we’d be glad to share the list with you. Just send me an email and I’ll put you on this list. In the meantime, here is a good article about the current delinquency situation – Click HERE

While we wait for inventory to build and the foreclosure market to appear we will continue to see a lot more of what we have seen. Most markets are experiencing fewer sales this year over last. At first, this was an inventory issue (can’t sell what’s not listed), but now that problem is being exasperated by higher interest rates (can’t buy what you can’t afford). The increasing prices will continue throughout the year.

Longmont Area Real Estate Stats May 2022 (pdf)

Longmont Area Real Estate Stats May 2022 (.jpg)

{kind=link}

Some notable items from around the region in this month’s report:

As inventory rises in both Longmont Single-Family and Attached Homes, Days on Market are also rising. This is what you are hearing in national publications. And they make it sound like the sky is falling. Inventories always rise at this time of year because this is the selling season and people want to sell their homes. Another misleading headline I could write is “Days on Market UP 23.1% over 2021!!” While this is true, it’s only gone from 24 days to 28 for single-family. The numbers are so darn low, a slight uptick appears to be a drastic increase. Guess what? Prices are also going up, so this is adversely affecting us how? It isn’t. It’s positive because we are having strong sales months now that we have inventory.

The Carbon Valley market is a touch different than Longmont this month. Its inventory isn’t rising and its days on market are still falling. Subsequently the monthly sales are low. Prices are still climbing at typical rates for the region. I have a long-winded theory that I won’t explain here, but I’d expect prices to level off out here before they do in Longmont. Give me six months or so and we should be able to see then.

This month’s guest market is Louisville. It recently become the 3rd Boulder County community to average over $1M. Just so you know, that $1.158M will buy you an average of 1,979 of finished square feet of housing. It’s a market that’s about 1/5th the size of Longmont and has suffered a recent loss of several hundred homes. Almost immediately after the Marshall Fire prices jumped to their current levels and have stayed here. I’m not sure if these prices are here to stay or if they will eventually drift lower in a year or so. It’ll be interesting either way. Louisville become the 3rd million-dollar community in Boulder County. Superior was about to break that mark just before the fire and has continued to rise since. Lafayette isn’t far behind, and Erie is in the mid-$800’s, so the best priced community in Boulder County is still Longmont.

This market has been called Savagely Unhealthy by Housing Wire. I agree. In the longer term, higher interest rates may end up being a blessing in disguise. Currently, high rates are making life difficult for those who need to buy now. Today the Fed is pumping the brakes on the economy, the effect in the real estate market will be flattening out of prices. We need this kind of break. Every day the cost of a house has been going up. If this were to stop for a while, more people could save and plan and buy a home tomorrow at today’s price. Here is another great article to support my position HERE.

You can’t change the market; you can only work with what you are given. Embrace the change.

Cheers,

Kyle Snyder

720-534-8355

firstamstats@gmail.com