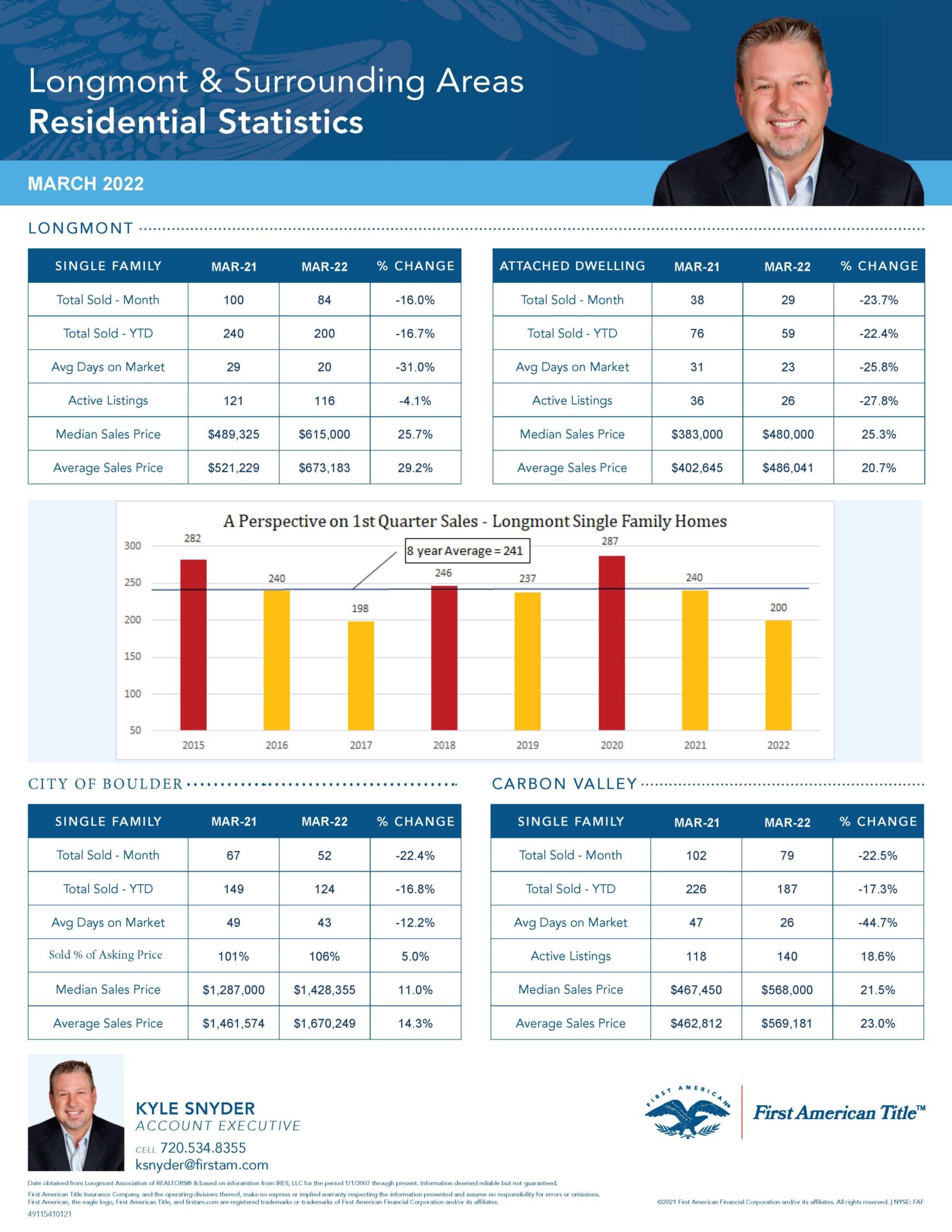

| When we were young, adults seemed so tall. When you bought your first home 20 years ago, it was a huge commitment and seemed so expensive. Now, adults don’t seem so tall, and that first home was no big deal and inexpensive compared to today. It’s because you are taller and make more money. Each observation is a snapshot in time. Your perception changed because your perspective changed. Our monthly stats reports are a snapshot in time. This past March is compared to March of the last year. Sometimes monthly results can seem extreme. Take April 2020 as an example…it was bad. It was also the start of lockdown AND the beginning of one of the best-ever years in real estate. This month’s report shows we closed 16% fewer homes last month than the previous March. It also says we’ve closed 16.7% fewer homes in the first quarter of this year compared to last. But where does that stack up against historical norms? Without perspective in the bigger picture, we don’t really know where we stand so let’s take a closer look. Over the past eight years, on average, 241 single-family homes closed in Longmont during the 1st Quarter. Including this year, five of the past 8 years have been below the average of 241. The three years, when there were 240, 240 and 237 closings, probably felt like darn average years. What about 2017? (Now is a good time to click on the report link below) Where was the concern when we had even fewer closing than this year? Where were the doom-and-gloom say-ers? They were taking a breath from the previous three, very lucrative, years. There was no doom coming from the lenders as they were busy refinancing the entire planet. Today, with both a slower pace of sales and rising interest rates (giving us a 70% decline in refinancing), both lenders and Realtors have time to ponder the future demise of the market. Why is this different than 2017? Longmont Area Real Estate Stats March 2022 (pdf) Longmont Area Real Estate Stats March 2022 (.jpg) We are still seeing increasing prices. We are still seeing fewer days on market. These are points of strength. They say there is strong demand from those who can afford it. Rising interest rates have surely eliminated thousands, or hundreds of thousands, from the pool of potential buyers. The difference between now and 2017 is that now there are only half as many homes for sale. Our lower sales total is a direct result of fewer homes offered for sale, but somehow the old bubble talk starts creeping back into the discussion…again. And by the way, I was right, no bubble burst and no foreclosure tsunami occurred. This time, again, no bubble. Too much equity. Demand is too high. And interest rates are still way below their historic average of 7%. Compared the past 10 years, rates seem high, but they aren’t. Perspective people. If you aren’t convinced yet. I added the stats from the City of Boulder to this month’s report. I didn’t do a square foot or bed/bath comparison, but I guarantee you the average home in Boulder, that’s 3X more expensive than the average home in Longmont, isn’t 3X bigger or 3X nicer. The extremely high cost of a home in Boulder is still pushing the demand and prices in Longmont. Speaking with clients recently, here are a few ideas when talking to buyers and sellers unwilling to participate in this market. Seller-Sell now if you think it’s a market top. Reap the rewards of your equity, rent for a couple years, and buy low when the market crashes. I don’t think it will, but if they are convicted in their stance, this is a good strategy. They can do the whole equity build thing again. Buyers-Would you still buy a home in Longmont for $250k back in 2008, knowing its value was going to drop 15% (to $212.5k) within two years? That same house is now $673k for a 2.7X gain. What’s it going to look like 14 years from now? It’s a real-life example of what recovery looks like. And this is WORST-CASE scenario, because the only thing worse than that recession was the Great Depression! Millennial Buyer-see above and ask if they’ve ever heard of Airbnb. They understand Airbnb, but not a long-term investment rental property even though they are the nearly the same thing. If they don’t put 20% down, they have a shot at building real wealth. Seller who asks, “Where do I move?”, give them this ARTICLE for ideas. Or refer to my extensive list of ideas from my JULY 2021 stats piece. Or show properties in Loveland and Greeley, the two most affordable town in the northern front range. |

{kind=link}